Overview: Meet the Company Sitting on $12 Billion in ETH

BitMine Immersion Technologies (NYSE American: BMNR) is a U.S.-listed company originally built around immersion-cooled Bitcoin mining and hosting infrastructure.

In June 2025, under the leadership of Chairman Tom Lee and CEO Chi Tsang, BitMine pivoted its corporate strategy, moving from a traditional mining business to a dedicated Ethereum treasury company.

An Ethereum treasury is a corporate strategy in which a publicly listed company holds ETH as its primary balance sheet reserve asset, making its valuation highly dependent on ETH price.

The idea is simple on the surface, concentrate exposure to a single digital asset at scale, but it raises a bigger question investors keep asking: can a company really build a durable business around holding a volatile token?

BitMine’s answer is that holding alone isn’t the business. Turning that treasury into a productive financial engine is.

Where the “Just Hold ETH” Plafybook Quietly Breaks

Corporate crypto treasuries sound compelling in a bull market but tend to reveal three structural weaknesses once volatility hits.

Passive treasury limitation: Digital asset treasuries (DATs) dominated by idle token holdings consistently trade at a discount to Net Asset Value (NAV), and price exposure alone does not translate into enterprise value.

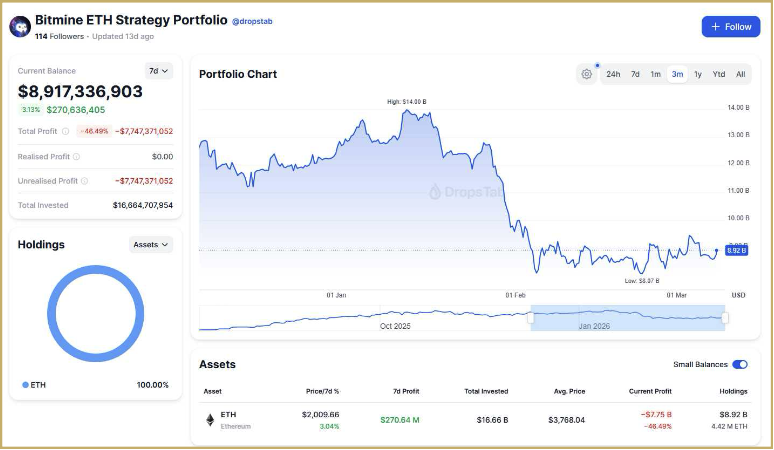

Volatility exposure: BitMine’s own ETH portfolio has swung from a peak near $14 billion down to the $8.7 to $9.0 billion range, with unrealized losses at one point exceeding $7.6 billion against $16.6 billion invested. Treasuries without offsetting revenue absorb those drawdowns directly into their market cap.

Lack of income generation: Spot ETH and spot ETH ETFs generate zero on-chain yield. A passive treasury leaves 3 to 5% native staking APY on the table, forgoes MEV rewards, and has no recurring revenue to cushion drawdowns.

BitMine ETH Strategy Portfolio chart from DropsTab

BitMine’s strategic pivot is about converting idle ETH into productive balance-sheet infrastructure. Instead of letting tokens sit in cold storage, the company is systematically layering multiple on-chain revenue streams on top of its holdings.

Staking

Over 2 million ETH actively staked (roughly 47% of total holdings).

Large staking tranches began late December 2025 and scaled rapidly into January 2026.

Network APY of 2.5% to 4% applied to a multi-billion-dollar base generates hundreds of millions in recurring pre-tax income.

BitMine’s in-house validator arm, MAVAN, is being built out to internalize validator economics.

The current phase relies on third-party operators while internal capacity scales.

Once live, MAVAN lets BitMine capture the full validator stack rather than sharing fees with external operators.

MEV & Builder Flows

On-chain data shows recurring inflows from major block builders, including Titan Builder, BuilderNet, and Quasar, into BitMine-labeled wallets.

These are consistent with MEV-boost reward flows, meaning MEV income is already being routed to the treasury.

Internalization through MAVAN is also expected to convert this from a third-party capture model to a fully owned revenue product.

On-Chain Revenue Streams

BitMine App: productized ETH exposure through on-chain savings/yield or structured tokenized products.

Tokenization: using ETH as input collateral for on-chain financial products.

DeFi and Layer-2 collaborations: extending utility and product reach.

Moonshot allocations: up to 5% of capital ($700M cap) reserved for strategic bets, including a $200M tie-up with Beast Industries and a $17 to $20M stake in Eightco Holdings (which holds exposure to Worldcoin).

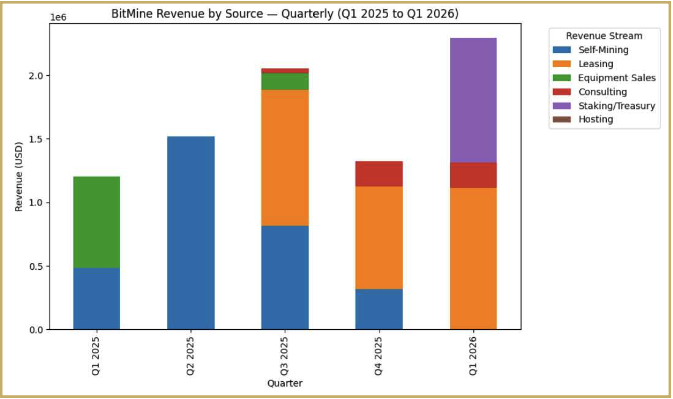

BitMine Revenue by Source (Q1 2025 to Q1 2026)

The Numbers Behind the Pivot

Income generation impact: Based on company disclosures, allocations of $13.1B to native ETH staking (at 2.8 to 3.0% yield) imply $367 to $393M in annual pre-tax staking income. Add $35 to $40M from $1B in short-duration cash instruments, and the total estimated pre-tax yield reaches $402 to $433M per year, before any MEV adjustments.

Business model shift: In Q1 2025, total revenue of roughly $1.2M was dominated by Bitcoin self-mining and equipment sales. By Q1 2026, revenue had climbed to $2.29M with the mix inverted:

$980K from staking/treasury operations.

$1.1M from leasing.

$2K from self-mining.

Within five quarters, staking went from 0% of revenue to becoming a primary driver.

Reduced dependence on mining: Self-mining revenue collapsed from $813K in Q3 2025 to $2K in Q1 2026. BitMine is no longer a mining company with an ETH treasury attached. It is an ETH operator with legacy mining exposure being phased out.

Market validation: BMNR returned 267% over the trailing 12 months versus -5% for spot ETH, outperforming ETFs like ETHA (+13.5%), FETH (+13.4%), and peers like SharpLink Gaming (+66%). Institutional ownership now includes BlackRock (over 9M shares), Charles Schwab, Morgan Stanley, ARK, and Vanguard.

Balance-sheet resilience: Crypto assets ($8.28B) cover total liabilities ($102M) by more than 80x. Stockholders’ equity of $8.69B across 24.1M shares implies a book NAV of roughly $360 per share.

Ethereum Treasury Holdings comparison, BitMine vs peers (SharpLink, The Ether Machine, Bit Digital, Coinbase)

The Bigger Takeaway

BitMine’s case study proves that the survival question for corporate crypto treasuries isn’t answered by accumulation alone. The companies that endure will be the ones that operationalize their token holdings into recurring cash flow through staking, validator infrastructure, MEV capture, and productized on-chain services.

For the broader corporate treasury trend, this indicates a shift away from the “buy and hold” DAT model toward a hybrid operator model where the treasury itself becomes the product. Passive holdings invite NAV discounts; productive holdings can command operating multiples.

For broader market context, explore Ethereum price prediction to understand long-term outlook scenarios shaping institutional positioning

BitMine’s scale, low leverage, and execution on MAVAN and its product roadmap put it in a position where balance-sheet failure would require a systemic collapse in Ethereum itself, rather than anything company-specific. That is a very different risk profile from a typical leveraged crypto company.

If this model scales as planned, it may become the blueprint for how corporate treasuries survive and compete moving forward.

For the full case study, including detailed scenario analysis at -30%, -50%, and -70% ETH price moves, on-chain evidence, and a practical checklist for other firms pursuing this strategy, download the complete CoinGape Research report.

Why trust CoinGape: CoinGape has covered the cryptocurrency industry since 2017, aiming to provide informative insights to our readers. Our journalists and analysts bring years of experience in market analysis and blockchain technology to ensure factual accuracy and balanced reporting. By following our Editorial Policy, our writers verify every source, fact-check each story, rely on reputable sources, and attribute quotes and media correctly. We also follow a rigorous Review Methodology when evaluating exchanges and tools. From emerging blockchain projects and coin launches to industry events and technical developments, we cover all facets of the digital asset space with unwavering commitment to timely, relevant information.

Investment disclaimer: The content reflects the author’s personal views and current market conditions. Please conduct your own research before investing in cryptocurrencies, as neither the author nor the publication is responsible for any financial losses.

Ad Disclosure: This site may feature sponsored content and affiliate links. All advertisements are clearly labeled, and ad partners have no influence over our editorial content.

Anas is a crypto editor at Coingape with 5+ years of experience covering cryptocurrency markets, exchanges, and digital asset infrastructure. His expertise spans crypto exchange reviews, trading platforms, crypto-friendly banks, and neobanks, with a strong focus on security, compliance, fees, and user experience. Anas applies rigorous editorial standards and data-driven analysis to ensure Coingape’s rankings and reviews are accurate, unbiased, and aligned with real-world investor needs.

Download Complete Report

April 2026

Want your project featured in a data-driven report or case study? Contact us at [email protected]

CoinGape is a burgeoning blockchain and crypto media company. It was recently awarded as the Best Crypto Media Company 2024 at Global Blockchain Show, Dubai. Our goal is to keep industry professionals up to date on the most recent news and developments. We are a team of experts who take great pride in offering unbiased and well researched information to help our readers make informed decisions. Read our Editorial Policy

Share