ByCoinGape

DATs:- The most accurate description of the first digital-asset treasury (DAT) companies is one few will use: a Soros reflexivity trade dressed as corporate strategy. Soros argued that price and fundamentals are not separate: a high enough share price changes what a company can do, which feeds back into the price as long as the operator keeps the loop turning.

Michael Saylor built that machine. A premium let Strategy issue equity above the value of its holdings; the proceeds bought bitcoin; the bitcoin reinforced the story; the story justified the next round. He ran it harder than anyone alive.

The imitators copied it with varying skill. Metaplanet, SharpLink and a long tail of others followed; many issued below the value of their own holdings and became wrappers around dilution, while a few built something real. But reflexive loops expire. Reflexivity is starting capital, not a business.

It ran on four premiums: access, interpretation, scarcity and cheap financing. All four are thinner in 2026 than in 2022, and eroding. Strip them away, and a company whose only product is its own share premium is in trouble. The loop reverses, and what compounded on the way up de-compounds on the way down.

Strategy and BitMine are no longer just reflexivity vehicles. Both saw the expiry coming and rebuilt, but not into the same thing.

Strategy is now a digital-credit engine on a bitcoin-heavy balance sheet. Bitcoin makes a near-pristine reserve asset, with no counterparty and continuous settlement; Saylor saw the financing implications early. Its preferred family, STRK, STRF, STRD and above all STRC, reaches investors who will never own a coin or touch MSTR common.

Despite the shorthand, STRC is not secured by Strategy’s bitcoin: the disclosures say the preferred securities carry only a claim on residual assets. What the bitcoin provides is economic backing rather than legal collateral. Strategy has put an unsecured credit stack on a hard but volatile reserve asset, and can raise against it while the market trusts the balance sheet.

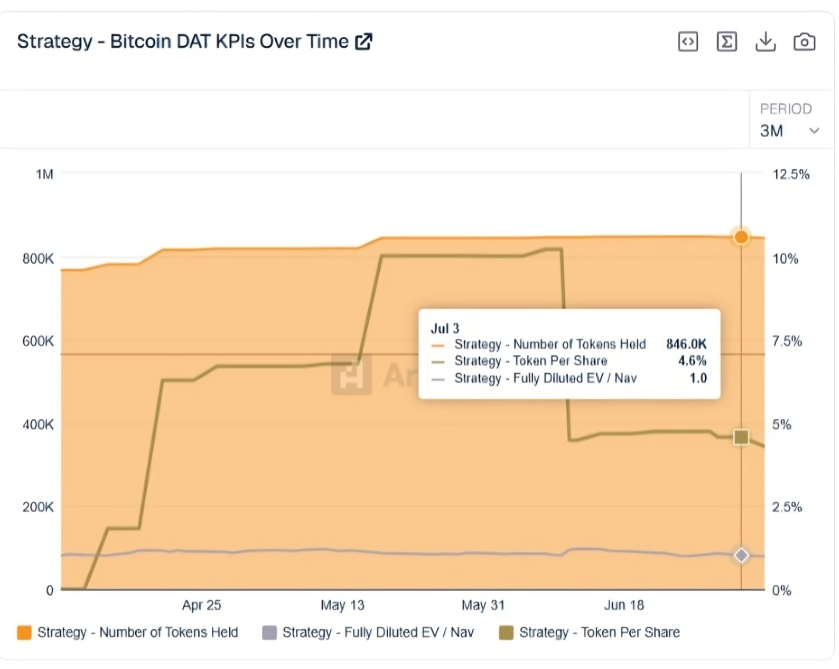

In late May it sold 32 bitcoin to fund distributions; a week later it bought 1,550 more, lifting its cash reserve to $1 billion. A treasury that both sells and buys to manage its book is no longer a “HODL” vehicle; it is doing asset-liability management.

Preferred has to be serviced, but it lessens reliance on a share premium, so the premium-to-NAV question matters less than it did. Saylor has built something close to a bank denominated in bitcoin.

BitMine took the other road. Its calling card is MAVAN, institutional staking infrastructure rather than a pile of tokens. Bitmine, a large staked-ether treasury becomes a productive asset throwing off cash flow.

This is the classic Berkshire move: Buffett’s edge came from operating cash flow and float, not stock-picking. Owning the company rather than the token means owning the machinery that produces the yield at scale.

Last month in June, it reached for Saylor’s other tool. It priced 3.5 million 9.50% perpetual preferred shares at $80 (about $273.8 million), listed on the NYSE as BMNP. A 9.50% coupon on a $100 stated amount sold at $80 costs close to 11.9% in cash, while staking yields sit in the low single digits. This is balance-sheet architecture, not a carry trade: capital raised to grow ether per share after costs.

The operating yield is real, but it does not make the cost of that capital disappear. STRC and BMNP open a DAT credit curve, each layer a claim judged on whether it raises digital assets per share. DAT 2.0 is less the end of reflexivity than its institutionalisation, the naïve premium loop giving way to a structured balance sheet.

However, neither a credit engine nor an operating-yield engine is the finished article. The complete version is Berkshire-shaped, a balance sheet running all three of Buffett’s engines at once: float, operations and allocation.

In crypto, digital float is a credit stack of perpetual preferreds and convertibles, digital operations are validators, staking, custody, market-making, and digital allocation is deployment across the ecosystem, all running on a reserve-asset treasury.

Strategy has the float and reserve but no operations. BitMine has operations and a reserve, and has just opened its own float, but is not yet an allocator. Nobody has built the synthesis, the form least exposed to any single premium compressing, because it spans more than one engine.

Which asset suits this form? Bitcoin fits the credit engine, where the asset is the product. Ether fits the operating company, where staking is the productive activity. The integrated form is harder to place: it rewards an asset that combines collateral utility, a yield surface, ecosystem cash flow and active deflation, and no single token owns all four cleanly.

Ether arguably touches most of them. BNB makes an even stronger case with deflationary supply. The aim is not to crown a winner but to note that the structure rewards breadth: whichever asset best combines the four needs the full Berkshire form, not a single engine.

Strategy has shown that a bitcoin balance sheet can become a credit engine, and that once it does, the operator stops being a believer and starts being an asset-liability manager. BitMine is showing that an ether treasury can become an operating-yield engine.

The third model is still unbuilt. Whoever builds it will be judged on one question: does each issuance, stake or dividend raise long-term digital assets per share, net of the leverage stacked on to get there? The companies that keep answering yes will matter more than those that simply own the most tokens or issue the most paper.

The easy Soros trade is over. The harder, Buffett-shaped version is what comes next.

Alex Odagiu

Alex Odagiu

Share