Buy $GGs

Buy $GGs2020 Ends With Banks Getting into DeFi, DeFi Startups Mimicking Banks

The notion that Bitcoin would one day wrest control away from the banking industry and grant financial sovereignty to the individual was percolating around cypherpunk internet forums soon after the protocol launched in 2009. Then, the summer of 2020 gave rise to the birth of decentralized finance (defi), and the idea of autonomous financial control took a hop, skip and a jump closer to fruition.

Yet, slowly creeping up on the cryptocurrency sector – and defi in particular – is a traditional finance industry that refuses to go down without a fight. Rather than be dismayed by the rise and rise of crypto’s newest products, traditional finance (tradfi) has adopted many of the tricks that defi gave rise to. Even as the defi market experienced a boom in 2020, in which transformative new products were launched, user metrics surged, and total value locked in (TVL) hit $12.4B, tradfi was moving at a similar pace.

Crypto Refines Finance

At the same time as fintech firms were adopting the products birthed in the crypto-realm, so too have cryptocurrency firms been refining some of the core elements of the existing finance industry.

For example, institutional-grade exchange AAX recently rolled out a savings product where users can earn interest on staked funds without a predefined lockup period, while accruing interest on their stake with every passing minute. By shifting such defi-centric staking features back onto centralized platforms, exchanges such as AAX are also attempting to finetune some of the ideas of defi, just like the fintech industry.

Instead of trading in the highly volatile #cryptocurrency market with high risk, #AAX savings allow you to grow your portfolio in a less risky environment.

Grow your #crypto holdings as a longterm investment with little effort, learn how here: https://t.co/QBt4Dgn3fh pic.twitter.com/dh31CMFqMM

— AAX (@AAXExchange) October 25, 2020

Meanwhile, crypto platforms such as Wirex and Revolut have converged with neo-banks, offering a mobile-first experience that mirrors the latter. While digital banking services such as Monzo don’t handle crypto, the user experience is now virtually indistinguishable. With PayPal having added the option for users to buy and sell cryptocurrency within its app, it’s hard to tell where tradfi ends and crypto begins. Further blurring the lines between the two sectors is Monolith, whose defi card allows users to self-custody assets before converting them into fiat at the push of a button, to be spent anywhere Visa is accepted.

Crypto: The Pioneer With an Arrow in Its Back?

The last decade of development in the cryptocurrency space has effectively been serving as a testing ground for the larger finance industry. Within just five years of Bitcoin’s launch, all of the major mobile payment apps that dominate the Western market (Apple Pay, CashApp, Samsung Pay) were announced and released to the public. The rise of mobile blockchain-based crypto-backed loans in 2017, and the three years of development since, has given yet more ideas to a burgeoning fintech industry that refuses to accept the axiom that it must use the blockchain if it wants to reap its fruits.

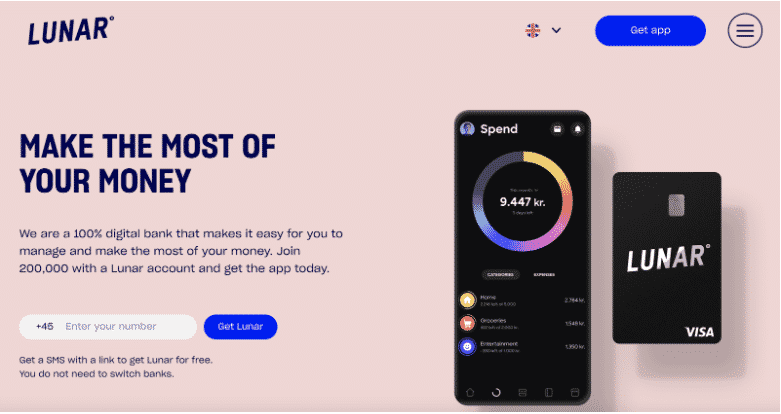

This has been witnessed in the rise of challenger banks, such as the Denmark-based Lunar, which recently raised $104 million in seed funding for its mobile banking app. Nearing the end of 2020, the sudden proliferation of challenger banks, bearing mobile-based banking apps that aren’t tied to any specific bank, have become a common sight to behold.

Even if challenger banks don’t necessarily represent the traditional finance sector (after all, they do compete with it), they do operate on similar terms. Banking licenses are required by these apps in any given jurisdiction, and their control and governance is still overseen by one or more trusted parties.

It’s not just a challenger bank play, however. Take for example Singapore’s largest, most-lauded bank, DBS, launching a crypto exchange with a promise to deliver a crypto trading experience, custodial services as well as security token offerings.

What’s undeniable is the fact that the fintech sector is undergoing its own revolution in absence of blockchain, even if some of its ideas were inspired by it. European company Klarna recently climbed to a $10.65B valuation, making it the biggest fintech firm on the continent. And like many of its competitors, it is already implementing ideas that would make much of the defi industry proud. Typical among these is the concept of Buy-Now-Pay-Later (BNPL), where applications allow users to make purchases in zero-interest installments from major online retailers, while gaining cash-back for punctual repayments.

Once, defi was expected to crash the traditional finance industry. Now, just months after its emergence onto the global stage, it is becoming harder and harder to distinguish blockchain-based applications from their non-blockchain counterparts. Autonomous financial control is still a pipedream for cypherpunks and crypto-anarchists. In the meantime, the traditional finance industry is quite happy to take from crypto and vice versa.

Play 10,000+ Casino Games at BC Game with Ease

- Instant Deposits And Withdrawals

- Crypto Casino And Sports Betting

- Exclusive Bonuses And Rewards

Why Trust CoinGape

CoinGape has covered the cryptocurrency industry since 2017, aiming to provide informative insights Read more… to our readers. Our journal analysts bring years of experience in market analysis and blockchain technology to ensure factual accuracy and balanced reporting. By following our Editorial Policy, our writers verify every source, fact-check each story, rely on reputable sources, and attribute quotes and media correctly. We also follow a rigorous Review Methodology when evaluating exchanges and tools. From emerging blockchain projects and coin launches to industry events and technical developments, we cover all facets of the digital asset space with unwavering commitment to timely, relevant information.

Delivered every day.

- Insights that move markets

- 100,000 active subscribers

Related Articles

- Senate Eyes CLARITY Act Markup This Month as Banks, Crypto Continue Stablecoin Yield Talks

- Why XRP Price Rising Today? (2 March)

- Breaking: Bitcoin Price Rises to $70k as Gold Crashes Amid U.S.-Iran Conflict

- Bitcoin News: Anthony Pompliano’s ProCap Buys 450 BTC, Gold Bug Peter Schiff Reacts

- Fed Rate Cuts More Likely If U.S.-Iran Conflict Extends, Arthur Hayes Predicts

- Top 5 Historical Reasons Dogecoin Price Is Not Rising

- Pi Coin Price Prediction for March 2026 Amid Network Upgrade, KYC Boost, Rewards Distribution

- Gold Price Nears ATH; Silver Eyes $100 Breakout on Us- Iran War

- Bitcoin And XRP Price As US Kills Iran Supreme Leader- Is A Crypto Crash Ahead?

- Gold Price Prediction 2026: Analysts Expect Gold to Reach $6,300 This Year

- Circle (CRCL) Stock Price Prediction as Today is the CLARITY Act Deadline