CoinGape has been covering cryptocurrency and blockchain markets since 2017. Our editorial team evaluates projects and platforms using structured review frameworks focused on transparency, utility, and risk assessment. You can explore our review methodologies to see how we assess and rate different categories. We maintain clear editorial standards and disclose advertising or affiliate relationships where applicable.

The DeFi lending and borrowing platforms are changing to meet demand and concentrate on extending credit without banks’ help. The demand for credit has increased, creating opportunities for passive income.

However, an increase in anything implies risk. This narrows down the options for selecting the best DeFi lending platform, which includes monitoring security, comparing APY and fees, and many other considerations.

Key Takeaways:

So, to save you time, we have researched and created a list of top DeFi lending platforms. This list is based on our review methodology, backed by real-world data and reliable sources, so you can make the right choice when picking a DeFi lending platform.

| Platform | APY (Average) | Supported Chains | Supported Cryptocurrencies | Interest Type | Ratings |

|---|---|---|---|---|---|

| 4-8% | Ethereum, Polygon, Avalanche | ETH, USDC, DAI, WBTC, and others | Variable/stable | 4.9 | |

| 3-6% | Ethereum, Base | ETH, USDC, DAI | Variable | 4.8 | |

| 3-5% | Ethereum | DAI | Stable | 4.7 | |

| 5-10% | Solana | SOL, USDC, USDT | Variable | 4.4 | |

| 7-12% | Ethereum, Solana | USDC, wETH | Fixed/variable | 4.5 | |

| 6-11% | Ethereum | ERC-20 tokens | Variable | 4.4 | |

| 5-9% | Solana | SOL, USDC, BTC | Variable | 4.2 | |

| 9-15% | Ethereum | USDC, TRU | Fixed | 3.9 | |

| 8-14% | BNB Chain, and Ethereum | Multiple Assets | Variable | 3.7 |

Our review of the best DeFi lending platforms highlights the best in the industry, examining their features, interest borrowers pay, security, and user experience. Whether you are a new investor or an experienced trader, understanding the strengths and weaknesses of these platforms would help you make informed decisions.

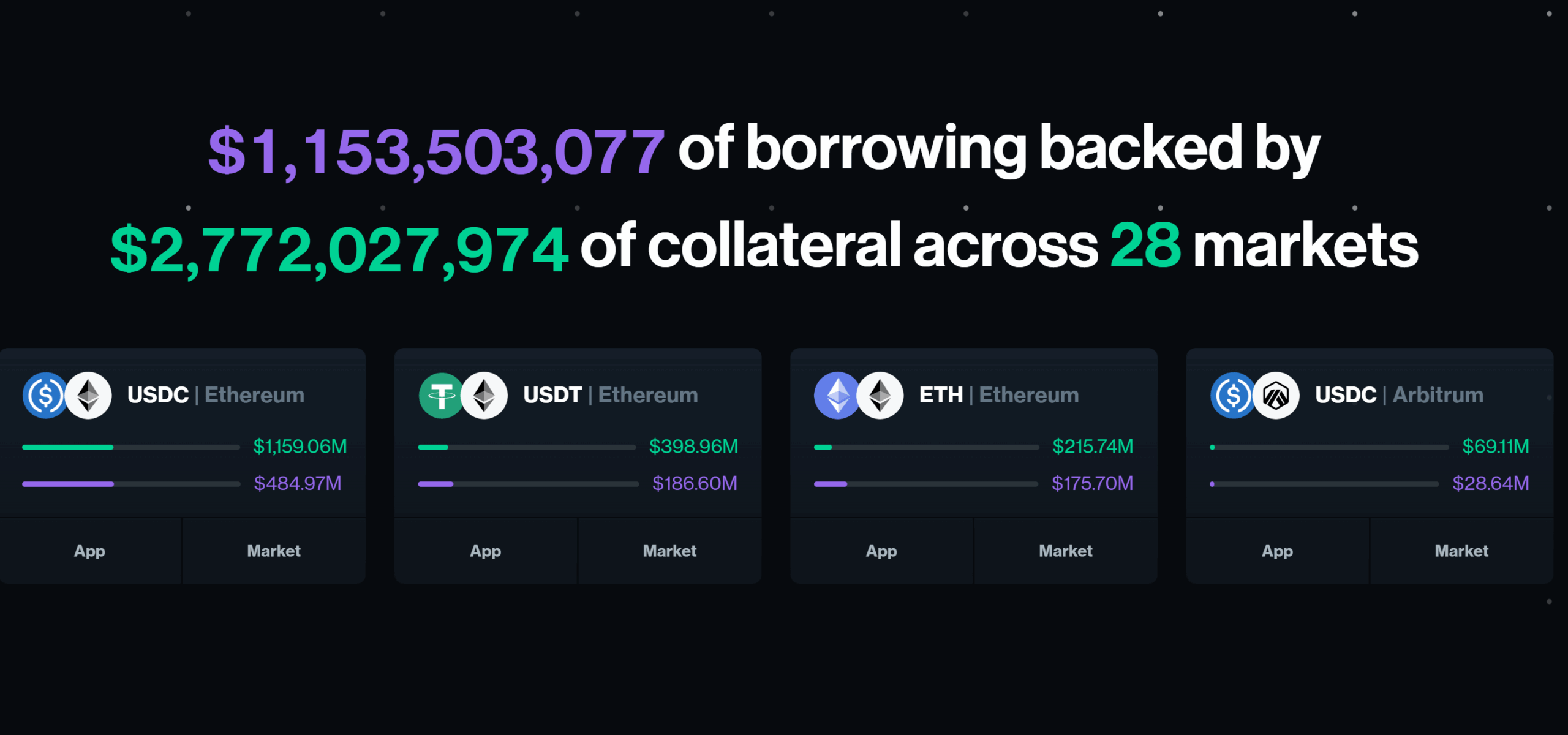

Aave, established in 2017 under the name Aave Companies but named Aave, is among the finest defi lending and borrowing platforms, where users can borrow and lend cryptocurrencies with no middlemen.

It is a lending platform on Ethereum, Polygon, Avalanche, Arbitrum, and Optimism, with a TVL of $10B (since Oct 2025). Users have an option of a stable or variable interest rate and receive rewards with the AAVE governance token.

The security of the platform is at the highest level, with frequent audits of smart contracts, integration with Chainlink, and working bug bounty programs.

Personal Experience:

Aave offers a smooth and open-ended lending experience where the yield is flexible and intuitive, and the platform is cross-chain-enabled. The dashboard is simple to operate for beginners, but at the same time, powerful enough to operate more advanced positions.

| Details | Information |

| Launch Year | 2017 |

| TVL (Oct 2025) | ~$10 Billion |

| Supported Chains | Ethereum, Polygon, Avalanche, Arbitrum, Optimism |

| Interest Types | Stable, Variable |

| Governance Token | AAVE |

| Unique Features | Flash Loans, Collateral Swapping, Real-time Health Factor, Cross-chain Portals, GHO Stablecoin |

Step 1: Connect Wallet

Link your MetaMask, Coinbase Wallet, or Ledger to Aave for secure multi-chain access.

Step 2: Deposit Collateral or Supply Assets

To Borrow: Deposit crypto such as ETH, DAI, or USDC. Borrowing power depends on the Loan-to-Value (LTV) ratio.

To Lend: Supply assets to liquidity pools and receive Tokens, which automatically accrue interest.

Step 3: Borrow or Earn

Borrow any supported token, yes, you can borrow and lend USDC with stable or variable rates. Carefully monitor your health factors to avoid liquidation. Earn APY and AAVE rewards, which adjust automatically based on market demand.

Step 4: Manage & Withdraw

Track positions via the dashboard. Borrowers can repay anytime, while lenders can withdraw principal plus interest once liquidity allows.

Compound Finance, which is among the best crypto lending DeFi platforms, was established in 2018 by Robert Leshner and allows users to lend and borrow cryptocurrencies without intermediaries.

It is a defi lending and borrowing software that supports Ethereum and Polygon and has a TVL of approximately $5B (Oct 2025). Borrowers are able to borrow at variable interest rates, and lenders provide assets to receive interest through the use of cTokens and COMP governance rewards.

Personal Experience:

Compound offers a user-friendly and automated experience. Interest rates are automatically adjusted, and thus users can gain competitive returns without having to manage their loans all the time. Altogether, Compound presents a balanced mix of ease and sophisticated functionality to both general and professional users of the DeFi.

| Details | Information |

| Launch Year | 2018 |

| TVL (Oct 2025) | ~$5 Billion |

| Supported Chains | Ethereum, Polygon |

| Interest Types | Variable |

| Governance Token | COMP |

| Unique Features | cTokens, Flash Loans, Algorithmic Rates, Governance Voting, Dynamic Rate Adjustment |

Step 1: Connect Wallet

Link MetaMask, Coinbase Wallet, or Ledger for secure access.

Step 2: Deposit Collateral or Supply Assets

To Borrow: Deposit crypto such as ETH, DAI, or USDC. Borrowing power depends on the Loan-to-Value (LTV) ratio.

To Lend: Supply assets to liquidity pools; receive Tokens that automatically earn interest.

Step 3: Borrow or Earn

Borrow supported tokens, including USDC, at variable interest rates. Manage your position to avoid liquidation. Earn interest and COMP rewards as the protocol dynamically adjusts rates based on supply and demand.

Step 4: Manage & Withdraw

Track positions through the dashboard. Borrowers can repay at any time, while lenders can withdraw principal plus interest once liquidity allows.

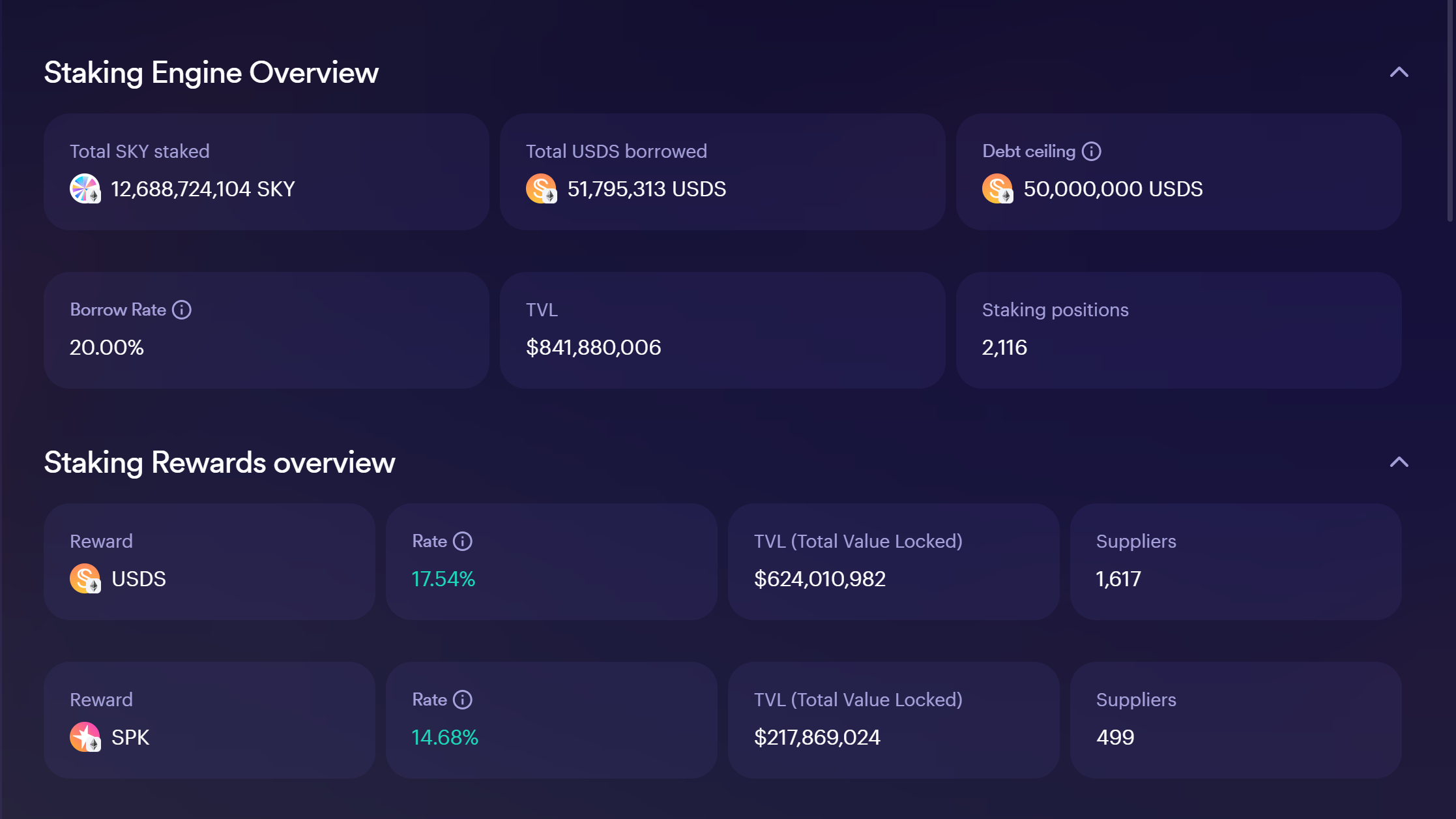

MakerDAO is a decentralized lending platform established in 2015 and supports the DAI stablecoin, allowing users to earn DAI by securing assets such as ETH and WBTC, and other qualified cryptocurrencies.

MakerDAO has a TVL of about 6B (Oct 2025) and provides multi-collateral support, and Stability fees and risk parameters are under the control of MKR token holders.

Personal Experience:

MakerDAO provides a reliable and transparent borrowing experience. Vaults allow users to generate DAI while retaining control over collateral, making it ideal for both new users and experienced DeFi participants. MakerDAO is particularly useful for those seeking predictable rates and risk-managed borrowing.

| Details | Information |

| Launch Year | 2015 |

| TVL (Oct 2025) | ~$6 Billion |

| Supported Chains | Ethereum, Arbitrum |

| Interest Types | Stability Fees |

| Governance Token | MKR |

| Unique Features | Multi-Collateral DAI, DAI Savings Rate, Governance MKR, Collateral Auctions, Vault Management |

Step 1: Connect Wallet

Use MetaMask, Ledger, or other supported wallets to access MakerDAO.

Step 2: Deposit Collateral

Open a Vault and deposit assets like ETH or WBTC. The Loan-to-Value (LTV) ratio determines borrowing capacity.

Step 3: Generate DAI

Borrow DAI against collateral. Monitor stability fees and the health factor of your Vault to avoid liquidation.

Step 4: Manage & Withdraw

Repay DAI anytime to unlock collateral. Use the dashboard to track positions and DSR earnings if you’re lending.

Solend is a defi lending and borrowing platform created in 2021 on the Solana blockchain that provides high-speed lending services, fast low-cost transactions, low-cost transactions.

It hosts stablecoins such as DAI and USDC, and other native tokens of Solana, and has a TVL of around $1.2B (Oct 2025). The dynamic interest rate model of Solend guarantees the right rates to the borrowers and lenders, and the platform is among the most decent crypto lending DeFi on Solana.

Personal Experience:

Solend provides an easy and friendly lending experience to users concerned with fast and low costs of transactions. Altogether, Solend is quite user-friendly as it combines easy accessibility with professional capabilities of DeFi users.

| Details | Information |

| Launch Year | 2021 |

| TVL (Oct 2025) | ~$1.2 Billion |

| Supported Chains | Solana |

| Interest Types | Variable |

| Governance Token | SLND |

| Unique Features | Dynamic Rates, Collateral Liquidation, Governance Voting, Solana Ecosystem Integration, Fast Transaction Processing |

Step 1: Connect Wallet

Use a Solana-compatible wallet like Phantom, Solflare, or Ledger for secure access.

Step 2: Deposit Collateral or Supply Assets

To Borrow: Deposit tokens such as SOL, DAI, or USDC. Borrowing power depends on the Loan-to-Value (LTV) ratio.

To Lend: Supply assets to liquidity pools and earn interest automatically.

Step 3: Borrow or Earn

Borrow any supported stablecoin, including USDC, with variable interest rates. Monitor your health factors to avoid liquidation. Earn APY and governance rewards for lending.

Step 4: Manage & Withdraw

Track all positions on the dashboard. Borrowers can repay anytime, while lenders withdraw principal plus interest once liquidity allows.

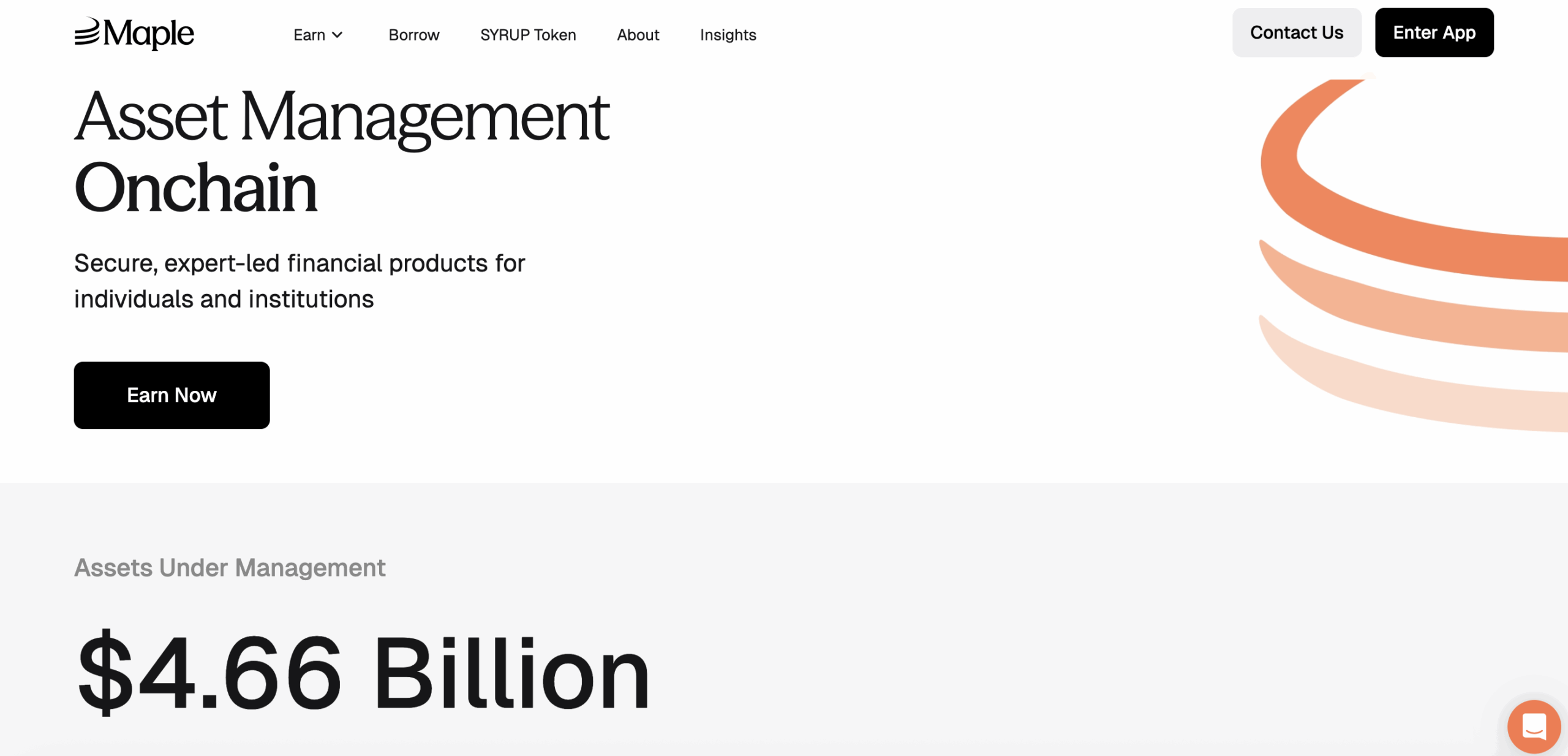

Maple Finance is a defi lending platform founded in 2020, aiming to offer institutional-quality lending in the DeFi ecosystem. It provides DAI, USDC, and other stablecoins, and it has a TVL of approximately $900M (Oct 2025). Maple Finance focuses on risk-traded loans with overcollateralization loans and vetting of borrowers to guarantee security and liquidity.

Personal Experience:

The institutional and large-scale investors that are concerned with risk management and security are the customers of Maple Finance. The credit pools offered on the platform enable lenders to provide funds and borrowers to take loans with easy terms. Follow-up and tracking of positions is easy, and the dynamic rates ensure that the lenders get good yields.

| Details | Information |

| Launch Year | 2020 |

| TVL (Oct 2025) | ~$900 Million |

| Supported Chains | Ethereum, Polygon |

| Interest Types | Variable |

| Governance Token | MPL |

| Unique Features | Credit Pools, Risk-Managed Lending, Governance MPL, Dynamic Rates, Institutional Focus |

Step 1: Connect Wallet

Use MetaMask, Coinbase Wallet, or Ledger for secure access.

Step 2: Deposit Collateral or Supply Assets

To Borrow: Deposit assets such as ETH or DAI; borrowing power depends on credit pool terms.

To Lend: Supply capital to credit pools and earn interest automatically.

Step 3: Borrow or Earn

Borrow DAI, USDC, or other supported tokens while maintaining collateral and pool requirements. Lenders earn interest, which adjusts dynamically according to pool demand.

Step 4: Manage & Withdraw

Track positions via the dashboard. Repay loans at any time; lenders can withdraw principal and interest when liquidity allows.

Euler Finance is a defi lending and borrowing platform established in 2021 to provide risk-isolated lending of different cryptocurrencies and stablecoins such as DAI and USDC.

Euler focuses on safety by using isolation mode, which isolates newly listed or high-risk assets and the broader protocol. The site has a TVL of approximately $450M (Oct 2025) and offers flexible collateral, which is why so many risk-averse DeFi users prefer it.

Personal Experience:

Euler Finance provides a very personalized and safe loaning framework. It is the best choice for both advanced and cautious users since its isolation mode ensures that risks of new or volatile assets do not impact the funds of other users.

| Details | Information |

| Launch Year | 2021 |

| TVL (Oct 2025) | ~$450 Million |

| Supported Chains | Ethereum |

| Interest Types | Variable |

| Governance Token | EUL |

| Unique Features | Isolation Mode, Flexible Collateral, Governance eToken, Risk Management, Dynamic Rates |

Step 1: Connect Wallet

Use MetaMask, Coinbase Wallet, or Ledger for secure access.

Step 2: Deposit Collateral or Supply Assets

To Borrow: Deposit ETH, DAI, or USDC. Borrowing power depends on the isolation pool and LTV ratio.

To Lend: Supply assets to selected pools; interest accrues automatically.

Step 3: Borrow or Earn

Borrow any supported token, including USDC, while monitoring the health factor. Earn interest on supplied assets, which adjusts dynamically to market demand.

Step 4: Manage & Withdraw

Track positions via the dashboard. Borrowers repay anytime; lenders withdraw principal plus interest as liquidity allows.

Port Finance is a defi lending platform that offers cross-chain liquidity and lending to stablecoins and other crypto assets such as DAI and USDC. Established in 2021, it gives support to Ethereum, Polygon, and Avalanche with a TVL of approximately 300M (Oct 2025).

Port Finance focuses on capital efficiency by enabling the free flow of liquidity through networks via networks, which makes it among the most suitable crypto lending DeFi platforms for users desiring to access the multi-chain.

Personal Experience:

Port Finance provides professional lending with enhanced cross-chain operations. It is easy to supply assets or to borrow USDC, and the active interest rates guarantee competitive returns. A well-organized and clear dashboard allows users to keep track of positions, LTV ratios, and health factors.

| Details | Information |

| Launch Year | 2021 |

| TVL (Oct 2025) | ~$300 Million |

| Supported Chains | Ethereum, Polygon, Avalanche |

| Interest Types | Variable |

| Governance Token | PORT |

| Unique Features | Cross-Chain Portals, Liquidity Pools, Governance PORT, Dynamic Rates, Multi-Chain Support |

Step 1: Connect Wallet

Use MetaMask, Coinbase Wallet, or Ledger for secure access.

Step 2: Deposit Collateral or Supply Assets

To Borrow: Deposit assets like ETH, DAI, or USDC. Borrowing power depends on the LTV ratio and network.

To Lend: Supply assets to liquidity pools to start earning interest automatically.

Step 3: Borrow or Earn

Borrow supported tokens, including USDC, while keeping an eye on your health factor. Earn interest on supplied assets, with rates adjusting based on pool demand.

Step 4: Manage & Withdraw

Track positions via the dashboard. Repay loans anytime; lenders can withdraw principal plus interest as liquidity allows.

TrueFi, which is an uncollateralized lending and borrowing platform, is a defi project created in 2020 that targets uncollateralized loans to vetted borrowers.

It allows the use of stablecoins such as DAI and USDC and other significant crypto assets, and its TVL is approximately 200M (Oct 2025). TrueFi is dedicated to credit risk evaluation in a way that it offers high-yield opportunities without jeopardizing lenders.

Personal Experience:

TrueFi is suitable for those users who are comfortable with greater risk in an attempt to have higher returns. It is easy to lend in USDC or DAI. The borrowers undergo a credit review.

The dashboard is easy to use with the display of loans, interest earned, and risk indicators. The uncollateralized model of TrueFi is distinctive in terms of the stablecoin Defi lending, which offers exceptional opportunities to yield-driven investors.

| Details | Information |

| Launch Year | 2020 |

| TVL (Oct 2025) | ~$200 Million |

| Supported Chains | Ethereum |

| Interest Types | Variable |

| Governance Token | TRU |

| Unique Features | Uncollateralized Loans, Credit Risk Assessment, Governance TRU, APY Optimization, Risk-Adjusted Lending |

Step 1: Connect Wallet

Use MetaMask, Ledger, or Coinbase Wallet to access TrueFi securely.

Step 2: Deposit Collateral or Supply Assets

To Borrow: Pass the credit assessment and deposit assets if required.

To Lend: Supply USDC, DAI, or other supported tokens to earn interest.

Step 3: Borrow or Earn

Borrow approved tokens, including USDC. Lenders earn APY, which adjusts dynamically based on credit pool performance.

Step 4: Manage & Withdraw

Track loans, repayments, and earned interest via the dashboard. Lenders can withdraw principal and earned interest anytime liquidity allows.

Cream Finance is a defi lending and borrowing platform that was established in 2020 and has multiple chains and supports stablecoins, such as DAI, USDC, and other crypto assets, including Ethereum, Binance Smart Chain, and Fantom.

Cream Finance is one of the most suitable crypto lending DeFi platforms to be used by multi-chain users, as it has a TVL of approximately $600M (Oct 2025) and offers flexible loaning and borrowing services with reasonable interest rates.

Personal Experience:

Cream Finance delivers a versatile lending experience for both retail and advanced DeFi users. Lending USDC or DAI is seamless, and borrowers can access multiple stablecoins with variable or stable rates. Cream Finance is particularly suitable for users looking for a combination of speed, flexibility, and multi-chain liquidity in 2025.

| Details | Information |

| Launch Year | 2020 |

| TVL (Oct 2025) | $600 Million |

| Supported Chains | Ethereum, BSC, Fantom |

| Interest Types | Stable, Variable |

| Governance Token | CREAM |

| Unique Features | Multi-Chain Lending, Flash Loans, Governance CREAM, Dynamic Rates, Risk Monitoring |

Step 1: Connect Wallet

Use MetaMask, Ledger, or Binance Wallet to access Cream Finance securely.

Step 2: Deposit Collateral or Supply Assets

To Borrow: Deposit assets such as ETH, DAI, or USDC. Borrowing power depends on LTV ratios and the network.

To Lend: Supply assets to liquidity pools to start earning interest automatically.

Step 3: Borrow or Earn

Borrow supported tokens, including USDC, with stable or variable rates. Earn interest dynamically adjusted to supply-demand balance.

Step 4: Manage & Withdraw

Track positions via the dashboard. Repay loans anytime; lenders can withdraw principal plus interest when liquidity allows.

DeFi (Decentralized Finance) lending is a system that is developed based on blockchains to allow individuals to lend out and borrow cryptocurrencies without the use of traditional financial institutions, such as banks. Smart contracts (computational segments on a blockchain) substitute trust, impose the rules, and automate transactions.

In case of an excessive fall in the value of the collateral (because of the market movements), it may be liquidated to cover the loan.

Let us assume that Alice possesses 10,000 USDC stablecoins. She puts them in a top defi lending protocol for stablecoins, with 8% APY (annualized). In a period of more than a year, she would be making about 800 USDC in interest, excluding fees.

Bob wants to borrow, yet he does not own a stablecoin but has ETH valued at 15,000. The protocol demands a Loan-to-Value (LTV) of not exceeding 66%. Bob puts on his ETH and takes out 9,900 USDC. He is anticipating that the stablecoin will be fixed.

Assuming that the ETH value fell at the time of his loan being taken out of $15,000 down to $10,000, now that the collateral only has a value of $10,000, yet his loaned sum and his interest may not be safe to carry on – his collateral can be sold off to settle. That’s Bob’s loss risk.

In case ETH increases or stays the same, Bob would be able to invest the borrowed USDC in other areas (e.g., in yield farming) and earn interest. But profit is a risky affair with the risk of liquidation, liquidity, fees, and volatility.

Here are all the different types of DeFi lending models:

When selecting a DeFi lending protocol, there are factors to consider and red flags to avoid.

| Factor | Why it matters? |

| APY (for lenders) / interest rate (for borrowers) | Determines how much you earn (or pay). Some platforms may offer high APYs but riskier collateral or stablecoins. |

| Loan-to-Value (LTV) ratio | Lower LTV means safer, but uses more collateral; higher LTV gives more leverage, more risk of liquidation. |

| Supported cryptocurrencies & stablecoins | If the platform supports many assets, you may have more flexibility. Also, stablecoins (less volatile) could reduce risk. |

| Security & audits | Good smart contract security, past audit records, track record, and reduce the risk of hacks or bugs. |

| Reputation & governance | Protocols with strong communities, transparent governance, and a good track record are more trustworthy. |

| Geographic availability / regulatory compliance | Some platforms may not allow users from certain jurisdictions; regulatory rules could affect your access or risk. |

| User experience (UI/UX), mobile app features | Ease of use of the platform matters; confusing interfaces or a poor experience increases the chances of mistakes. |

| Fees (withdrawal, gas, transaction, hidden fees) | Even if the interest looks good, high fees may reduce net returns. |

| Liquidation mechanism & grace periods | How and when the protocol liquidates should be fair; soft liquidation or buffer periods help reduce loss. |

| Loan processing speed/flexibility (stable vs variable rates, fixed durations, etc.) | Some platforms give you stable rates or allow flexible repayment. These options matter depending on your strategy. |

Below is how we (as content reviewers) rated the platforms that we cover. These are the criteria, and what each of them entails in practice.

Here’s how we did it:

Our review of every platform is based on this rubric, whereby we gather information (past performance, user reviews, audited code, historical liquidations), then rank/score them using that information.

DeFi Lending Platforms – DeFi lending platforms are smart-contract-based networks that are decentralized, where lending/borrowing occurs on a peer-to-peer or pool basis, and the funds are not directly controlled by a central institution.

CeFi Lending Platforms – Centralized lending platforms (CeFi) are operated by business entities; they control user money, apply KYC/AML (Know Your Customer / Anti-Money Laundering), are regulated, and can have greater control over interest rates, risk operations, collateral, etc.

Here is a comparison:

| Feature | DeFi Lending Platform | Centralized Lending Platform |

| Control / Custody | Users retain custody of their own crypto (wallets), and collateral is managed via smart contracts | The platform holds users’ funds; users trust the entity with custody |

| Trust & transparency | Code is usually open-source; terms are enforced by smart contracts; audit history is visible | Rely on company policies; less transparent; risk of mismanagement |

| Regulation & compliance | Often operate in loosely regulated or uncertain legal environments; some try to comply | Must follow many regulations, KYC, AML, licensing |

| Access / Onboarding | Usually easier, pseudonymous wallets; minimal KYC in many cases | Strict KYC, identity verification, and sometimes geographical restrictions |

| Interest rates & APYs | Rates can be more volatile; high yields are possible because of automated supply/demand, sometimes more favorable for participants | More stable rates, but often lower; risk management tends to reduce extremes |

| Liquidation risk | High if collateral volatile; mechanisms vary; may be automated and harsh | Usually more conservatively managed; risk models may allow more buffer; sometimes more manual intervention |

| Innovation & features | Flash loans, composability, tokenization of real-world assets, cross-protocol integrations | Slower innovation; risk-focused; less willingness to integrate risky/new models |

| Fees & hidden risks | Gas fees, smart contract risk, oracle risk, risk of protocol hacks | Credit risk, but less smart contract risk; fees are more explicit but possibly higher for intermediaries |

Future potential: There might be more hybrid forms (regulated, to some extent) where platforms have DeFi functionality with controlled oversight; and there could be international standards or frameworks.

Yes. it’s one of the best prospects. This is where RWAs (Real World Assets) come in, which platforms are performing, and what the risks/opportunities are.

To the ones who are not comfortable using their crypto as collateral or taking risks in DeFi, there are other alternatives:

Here are the drivers now and emerging trends in the defi lending space in 2025 and beyond:

Lending goals primarily assist in selecting the appropriate DeFi lending platform, which also reduces risk. However, an important factor of security outweighs any flashy APYs. A platform’s longevity, community audits, and governance model must also be taken into account.

As per the list mentioned above, Aave falls in the category of best for retail investors. For institutional investors, Maple Finance offers collateralized pools and fixed income. For beginners, Euler Finance is likely to be a good option, as it provides multi-token lending and algorithmic interest rates. MakerDAO is best for businesses and stable yields.

The DeFi lending ecosystem has improved dramatically in recent years, but would still demands due diligence before investing.

Aave, Compound and Crypto.com are solid starting points for new users because they combine clear interfaces, strong liquidity and lots of beginner guides. If you prefer lower fees, look for platforms on Layer-2 networks (like Optimism) or BSC-based options. Try a small test deposit first to learn the flow before committing larger sums.

Platforms like Compound and MakerDAO use audited smart contracts, but risks like code vulnerabilities and market volatility remain. Always research security measures.

Choose platforms with high APYs (e.g., Crypto.com, Synthetix) and diversify across stablecoins and volatile assets to balance risk and reward.

Most DeFi loans require over-collateralization, meaning you lock up more value than you borrow. The main exception is “flash loans” (Aave popularized these), which allow zero-collateral borrowing only if the loan is repaid within the same blockchain transaction. This tool is mainly for developers and traders, not everyday borrowers.

Rates are set algorithmically and change with supply and demand. It means that when more people want to borrow an asset, its borrowing rate rises. Similarly, when more people supply it, yields fall. Other factors that shape how rates react to market changes include protocol design.

Over-collateralization means pledging more value than the loan you take. For example, posting $150 of ETH to borrow $100 in stablecoins. That extra commitment protects lenders and the protocol if collateral drops in price, reducing the chance that the loan can’t be repaid.

You should watch for smart-contract bugs, oracle failures, sudden price drops that trigger liquidation, and front-running or MEV attacks. Operational risks such as rug pulls, governance attacks and gas spikes that make emergency moves expensive are also common pitfalls.

Check for recent third-party audits, a public bug-bounty program, on-chain transparency (proof of reserves), and active developer activity on GitHub. Read community threads and incident history. If a protocol has repeated security incidents, tread very carefully.

DeFi is non-custodial. As a result, smart contracts manage loans and you keep custody of assets. On the other hand, CeFi platforms (exchanges and lenders) hold custody, run their own risk models, and usually require KYC. DeFi gives more control and transparency; CeFi offers fiat rails and often simpler UX.

Gas fees depend on the underlying chain. For example, Ethereum mainnet transactions can be costly during congestion. As a result, many platforms now support Layer-2s or alternative chains to lower fees. You’ll usually pay gas for deposits, withdrawals and loan adjustments.

50k+ Articles

50k+ Articles