Breaking: U.S. SEC Charges Another Leading Crypto Exchange; Platform Forced To Shut Down

The Securities and Exchange Commission (SEC) has brought charges against the cryptocurrency platform Beaxy as well as its executives, alleging that they failed to register as an exchange, broker, or clearing agency. This comes as the latest action taken by the financial watchdog in their ongoing rampant crackdown on crypto firms operating in the United States.

SEC Charges Beaxy Crypto Exchange

The Chicago-based Beaxy Digital Ltd. was also charged by the SEC of fraudulently raising $8 million through its sale of unregistered security with its BXY token. In addition, the SEC also charged founder Artak Hamazaspyan for misappropriating funds worth $900,000 in personal use, including gambling.

Read More: Will This New Development Propel BNB Price To New All-Time High?

Along with Artak, two other executives Nicholas Murphy and Randolph Bay Abbott were also implicated in the lawsuit because of a company that they oversaw called Windy — which was responsible for maintaining Beaxy. According to the SEC’s allegations, Windy breached securities laws by transacting business through the Beaxy platform without first registering either as an exchange, a clearing agency, or a broker.

Beaxy Shuts Down Services

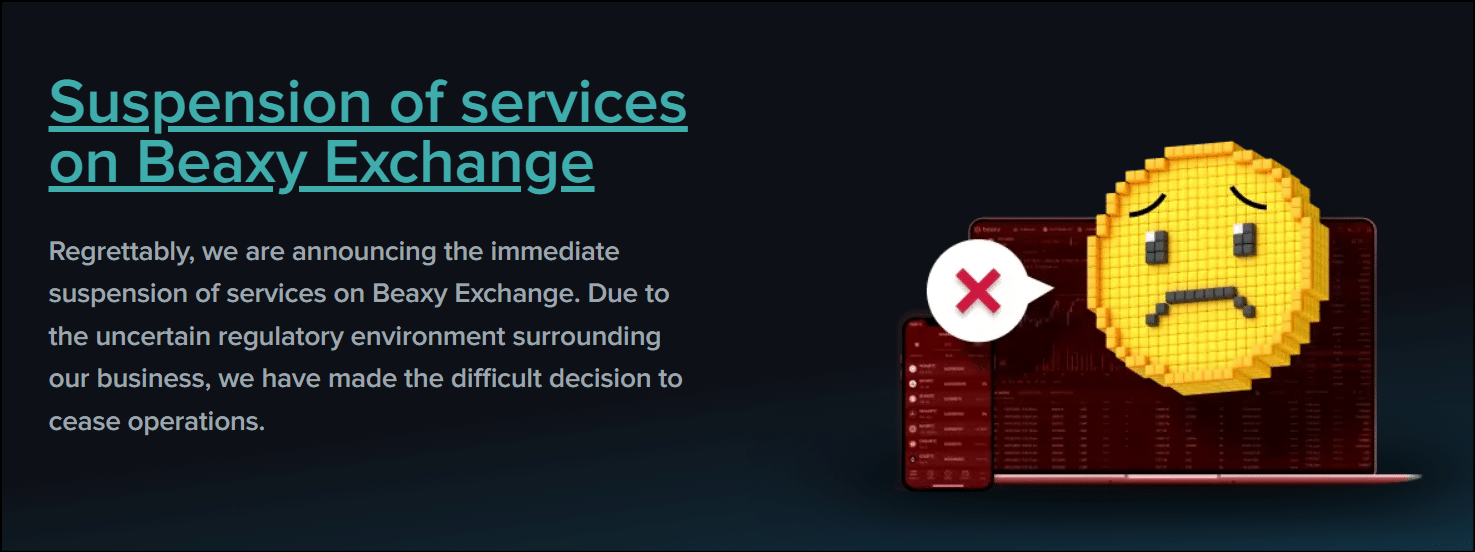

Following the lawsuit, the crypto exchange announced its decision to immediately halt operations via a post on its website, citing the “uncertain regulatory environment surrounding our business” as the reason for the abrupt move. As a direct consequence of this, the utility of the platform’s native token, BXY, has been lost, leaving investors in distress.

While speaking about the continuing crackdowns on several crypto firms including Beaxy, SEC chief Gary Gensler was quoted as saying:

This case serves as yet another reminder to crypto intermediaries that their business models must comply and adapt to the law, not the other way around.

According to Beaxy’s official statement, customers of the exchange have the ability to withdraw their funds within 24 hours following the closure of all open orders and balances being verified. The accused individuals have not admitted or denied the allegations leveled against them by the agency.

Also Read: Bitcoin Price Reclaims $28,500 Amid Binance FUD, Here’s Why

Why Trust CoinGape

CoinGape has covered the cryptocurrency industry since 2017, aiming to provide informative insights Read more… to our readers. Our journal analysts bring years of experience in market analysis and blockchain technology to ensure factual accuracy and balanced reporting. By following our Editorial Policy, our writers verify every source, fact-check each story, rely on reputable sources, and attribute quotes and media correctly. We also follow a rigorous Review Methodology when evaluating exchanges and tools. From emerging blockchain projects and coin launches to industry events and technical developments, we cover all facets of the digital asset space with unwavering commitment to timely, relevant information.

Delivered every day.

- Insights that move markets

- 100,000 active subscribers