Why DeFi aka Decentralized Finance Is a Must Know Crypto Trend For Every Finance Professional?

Decentralized Finance, popularly known as DeFi, is another disruptive application of blockchain technology enabling more people across the globe to access financial services. It refers to digital assets and financial smart contracts, protocols, and decentralized applications (DApps) built on blockchain technology, more specifically, Ethereum. In this blog, we will explore the following aspects of DeFi –

- Centralised Finance vs Decentralised Finance

- Types of DeFi Products in the market

- Size of the DeFi Market

- Pros and Cons of Decentralised Finance

- Future of the DeFi market

Why: Issues With Traditional Finance?

Traditional finance is marked by centralization. It is controlled by centralised institutions that decide who gets access to financial services and who does not. For example, to avail of a loan, one must have a bank account and a sound credit score. To have a bank account, the person should have fulfilled the bank’s KYC procedures. Someone who doesn’t have the necessary KYC documents cannot open a bank account, and therefore cannot avail of a loan or get access to other banking services such as a credit card, foreign currency exchange, Demat account, online payments, etc.

Therefore, traditional finance is characterized by strict parameters that tend to exclude a large chunk of people, especially in developing countries, and deprive them of participating in activities involving the creation of economic value.

Traditional finance is also fundamentally flawed in another respect – it is centralised, and therefore, a massive amount of power rests in the hands of institutions. We have to trust these institutions with our assets. But, the economic crisis of 2008 is a reminder of the fact that centralizing power is risky.

Even regulated financial institutions, despite their stringent checks around to whom they decide to give money, are not infallible. For instance, banks may advance unsecured loans to a large number of people or companies who are unable to repay the loans. In such a case, banks, in many countries, have access to a resolution called a bail-in. In a bail-in, a troubled bank is provided relief by the cancellation of its debts to creditors and depositors. This implies that the bank can use the money of consumers to get out of distressed situations.

How Defi will help?

The bottom line is that the problems with centralised institutions are many, and the need to switch to DeFi can’t be overstated. DeFi, though still in its early stages, has disruptive potential. If allowed to prosper, it can replace many legacy systems in finance. At present, it is already enabling people to gain access to a wider range of financial services, irrespective of the country of their origin, their financial status and other traditional parameters. Anyone with an internet connection can access DeFi products built on the Ethereum blockchain.

DeFi is also giving people an alternative to relying on traditional, centralised financial institutions. Since DeFi uses blockchain, users interact with decentralized architecture while accessing DeFi products. Secondly, there is more transparency about transactions in the DeFi ecosystem as all transactions are recorded on the blockchain and are available for public scrutiny. Thirdly, the funds of users are controlled by smart contracts and not companies.

According to Alex Pack, managing partner at Dragonfly Capital, a $100 million crypto fund,

“The goal of DeFi is to reconstruct the banking system for the whole world in this open, permissionless way,”

Sahil Deshpande, a partner at Bain Capital Ventures echoes similar views about DeFi. He says –

Decentralized financial applications “can make our financial systems more transparent, more resilient and less fragile,”

Types of DeFi Products

In order to understand DeFi in-depth, it is important to understand its products. One thing is common between all the products – they are based on blockchain-powered open protocols. Most of the existing products are based on the Ethereum blockchain, except for one that is on the Bitcoin blockchain. Let us look at some DeFi product categories –

-

Lending

In Lending, users can borrow one asset by giving another asset as collateral. The collateral is usually ETH, and the borrowed token depends on what the firm is offering. The debt has an accruing interest which is to be paid off when along with principal interest.

Maker, a lending DeFi product, offers its USD-backed stablecoin DAI, when ETH is given as c0llateral. The value of the collateral is always higher than the value of the loan to ensure that in the case of a non-repayment of the loan, the collateral can be used to cover up the lender’s loss. In the case of Maker, users can borrow up to 66% of value in DAI on the collateral they lock-up.

In case the value of the collateral falls below the stipulated rate, then the lender may impose a penalty on the borrower and even liquidate their collateral in the open market. Maker charges a 13% penalty if the value of the collateral falls below the 150% collateralization ratio and also sells the collateral at a 3% discount in the open market.

Giving Maker strong competition is EOS’ stablecoin initiative for crypto lending. The USD-backed stablecoin, EOSDT, leverages EOS’ collateral to add to the liquidity in the market. A user can simply lock up their digital assets to issue EOSDT. The level of collateralization is 130%, lower than other lending products in the market.

There are several DeFi lending products in the market which follow a similar model of lending. Compound allows users to supply assets to its liquidity pool and earn compounding interest on that. From this pool, it lends assets to borrowers at interest. dYdX allows borrowers to take leveraged long positions of up to 4x their collateral value or leveraged short positions of up to 3x of their collateral value.

-

Derivatives

Derivatives are another class of DeFi products – derivatives can range from asset-backed tokens to alternative insurance to decentralized oracles or p2p protocols for prediction markets.

For example, Synthetix is a decentralized platform that allows for the creation of Synths – assets based on fiat currencies, commodities and crypto-assets. Ethereum-based Nexus Mutual allows members to pool and share risk through a community-owned insurance alternative called a discretionary mutual. Augur is a decentralized, p2p protocol that allows users to create a market around the outcome of any event and bet on it.

-

Dexes

Dexes are open protocols, which, instead of relying on order books, use liquidity pools for token exchange. In simple terms, they facilitate the exchange of crypto assets using smart contracts deployed on the blockchain using liquidity pools. The trading rules are coded into smart contracts deployed on the Ethereum blockchain.

Uniswap is an example of a DEX which allows anyone to create a market or a liquidity pool by providing an equal value of ETH and an ERC20 token. The exchange rate is initially set by the creator of the market, but it keeps changing as trading takes place and the liquidity of one asset compared to the other gets reduced. The arbitrage opportunities presented by these changes promote more trading.

Bancor, like Uniswap, also uses pooled liquidity instead of order books for token exchange. Bancor uses “smart tokens”, which can be considered as tokens that hold the monetary value of other cryptocurrencies. In other words, smart tokens hold the reserves of other ERC20 tokens and are linked to smart contracts. On the exchange, smart tokens are used internally for converting from one asset to another depending on reserves of the tokens.

Kyber is another on-chain liquidity protocol that facilitates token exchange with the help of reserves. Users can create token reserves, which will exist as smart contracts on the Kyber network. When a user wants to exchange a token, Kyber will check across all reserves and show the best price.

-

Assets

Assets are another class of DeFi products. In this category, there are different types of product offerings – sets of tokens as an investment, tokens backed by other tokens and decentralized asset management.

Set Protocol offers tokens that represent other underlying assets or sets of tokens, for example, ETH and USDT, clubbed together in a specified proportion. Consumers can buy TokenSets based on different strategies – trend trading, range-bound, and buy and hold. For e.g. in Trend trading, if you are holding a token representing ETH and USDT which rebalances according to 20-day moving average, then your token set will be 100% ETH is the price of ETH is above the 20-day moving average, and it will rebalance to USDT if the price goes below the 20-day moving average. The process of rebalancing will be governed by a Smart Contract.

WBTC is an ERC20 token backed by BTC in 1:1 which can be traded on DEXes which support ERC20 tokens. The idea behind yolking Bitcoin and Ethereum together are to bring Bitcoin’s vast liquidity into Ethereum. The token is helping in the expansion of both the networks. For example, this token helps in utilizing DEXes for trading BTC.

Melon Protocol facilitates decentralized asset management. It enables anyone to create their own asset fund whose rules are coded into the smart contract, thus, lowering the barriers to entry into asset management. It also helps investors evaluate different asset funds available in the Melon network and invest in them at a fraction of the cost of what they would pay to traditional asset managers.

-

Payments

Payments are an interesting use-case of decentralized finance with products that utilize both Bitcoin and the Ethereum blockchain. In the payments sector, DeFi products have tried to make micro-payments more efficient and inexpensive, thereby improving the scalability of blockchain networks.

Lightning Network is a product focusing on Bitcoin blockchain which induces efficiency in smaller transactions by taking them off-chain. In the Lightning Network, two or more network members who want to transact can open a channel by depositing funds. They can perform as many transactions as they want without exceeding the amount of the funds deposited. All transactions will be recorded off-chain, and when the channel is closed, the most recent state of the off-chain ledger will be updated on the blockchain.

xDAI Chain is a payment solution with a 5-second block time and very gas fee. It an Ethereum sidechain that uses the Proof of Autonomy (POA) consensus algorithm. In POA consensus algorithm, only US public notaries can become validators and are managed by a Decentralised Autonomous Organisation (DAO). In the xDAI network, xDAI tokens, backed by DAI in a 1:1 ratio, have the same role as ETH does in the Ethereum network.

Connext is another DeFi product related to payments. Like the Lightning network, it too uses an off-chain solution for fast, low-cost micropayments. Connect requires it users to set up a Dai card that hosts an Ethereum wallet. The Dai card can be loaded for up to $30 with ETH or DAI. The Dai cardholder can then send micropayments to any other user with a Dai card.

Now, let us look at how DeFi products are performing in the market.

DeFi Statistics – How Big is This Market Presently?

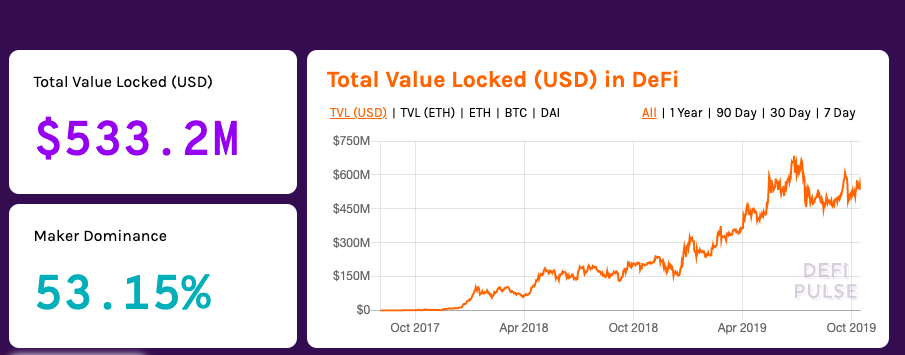

According to DeFiPulse, a total of $531 MM is locked in the DeFi market presently. There are a total of 20 DeFi products belonging to different categories – Lending, Derivatives, Dexes, Assets, and Payments. MakerDAO is the largest DeFi product with a market share of over 53% and funds worth $281.8 MM locked in. Compound and Synthetix are the second and third largest products with locked-in funds worth $106.3 MM and $59.7 MM respectively.

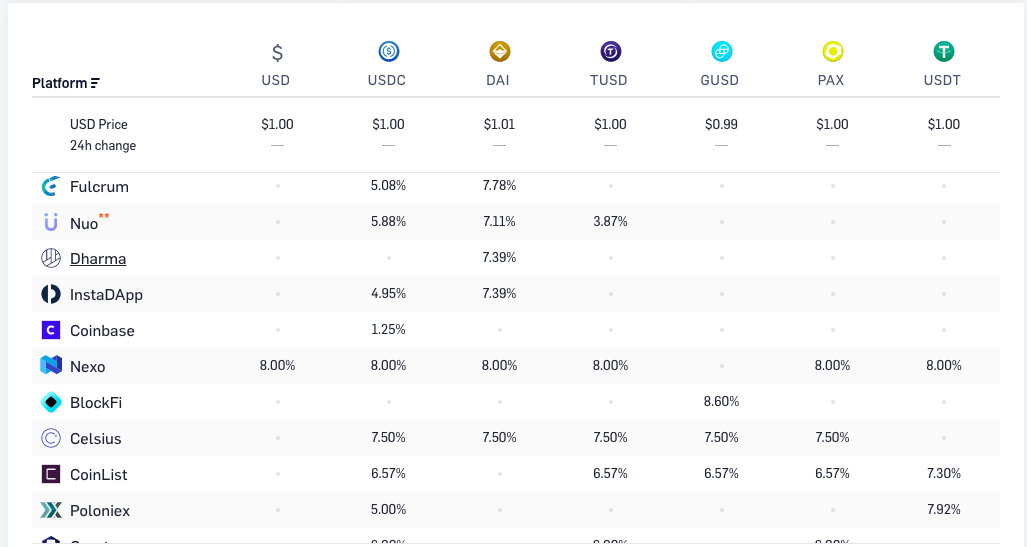

LoanScan is a website that shows the top lending products in the crypto world. Compound, dYdX, Dharma, InstaDApp and Nuo are among the leading DeFi products which enable crypto users to earn interest on their crypto holdings.

Pros and Cons of DeFi

The pros of DeFi are many.

- First of all, it promotes financial inclusion as barriers to accessing DeFi products are low. People from across the world can participate in utilizing DeFi products. For example, people can access DeFi assets without needing tens of thousands of dollars. They can exchange tokens on DEXes without having to perform KYC. They can borrow tokens without having a bank account.

- Secondly, DeFi products are decentralized and controlled by a smart contract. In other words, a centralised authority doesn’t have control over your funds, though it might be the builder of the product. Thus, users can access DeFi products and put their money in them without having to trust a centralised authority.

- Thirdly, DeFi products are contributing to the crypto ecosystem by creating new forms of value and expanding the use cases of cryptocurrencies. Thus, DeFi products are helping the crypto ecosystem grow and diversify.

- Fourthly, they are also solving several problems in the crypto ecosystem. For example, DeFi payment products are helping in making micropayments quick, inexpensive and easy. DEXes are trying to solve the problem of liquidity in the crypto market.

- Last but not least, DeFi is driving innovation in the cryptosphere. People can create their own products, whose rules will be embedded into a smart contract, and offer them to other people. Network effects will not only help in the adoption of these products but also lead to the creation of new products.

DeFi also has several drawbacks, some of which were fixed, and there are others that can’t be fixed.

- Firstly, not all products have low barriers to entry. Lending is a product class in which the user needs to have a high amount of ETH for collateralization of the debt. The ETH is prone to get liquidated if the value of the collateral falls below a certain level.

- Many DeFi products are only partially decentralized as the companies creating them are centralised and they create rigid rules around the product. However, the good news is that these companies don’t own your private keys. Also, in many cases, only a step of the process is decentralized. For example, if you need ETH for accessing a particular product, it is likely that you will be purchasing that ETH on a centralised exchange.

- About Smart Contracts, they are not 100% secure. Though deployed on robust blockchains that are virtually impossible to be hacked, smart contracts themselves may have bugs that can be exploited by hackers to drain out all your funds. A very infamous example of this is The DAO attack.

- Finally, DeFi products suffer from the same problem that the entire world of crypto does – complexity. For most people, crypto is hard to understand, which is why they still haven’t been able to embrace it. The same now goes for DeFi products as well – their connection with crypto, while on one hand, it makes them unique and disruptive, on the other handle, it becomes a hurdle to their adoption.

The Future of DeFi

Well, despite all the problems, does the future of DeFi look bright? Sure it does! DeFi is still at an early age – its size is a tiny fraction of the size of the crypto market. However, it has stirred the interest of the crypto community and it is evolving – one step at a time. From $4 in August 2017 to over $680 MM in June 2019, DeFi has shown massive growth in just 2 years. As the crypto industry grows and gains adoption, DeFi is also likely to see an increase in value with more participants moving to DeFi.

In fact, the DeFi movement is already adding more blockchain networks. EOS has established itself as a major player with EOSDT. Tron has also joined the DeFi movement, as it announced its partnership with the Loom Network in September. With the help of Loom Network’s solutions, it will be able to deploy MakerDAO’s DAI stablecoin on the Tron blockchain.

Given the rapid developments and the growth in the world of DeFi, and the mainstream adoption of crypto, it is a possibility that DeFi may overtake traditional finance in the future.

What do you think of the future of DeFi? Do you think it has disruptive potential, or is it just a bubble? Share your views with us in the comments below!

[post_grid id=”32220″]

Why Trust CoinGape

CoinGape has covered the cryptocurrency industry since 2017, aiming to provide informative insights Read more… to our readers. Our journal analysts bring years of experience in market analysis and blockchain technology to ensure factual accuracy and balanced reporting. By following our Editorial Policy, our writers verify every source, fact-check each story, rely on reputable sources, and attribute quotes and media correctly. We also follow a rigorous Review Methodology when evaluating exchanges and tools. From emerging blockchain projects and coin launches to industry events and technical developments, we cover all facets of the digital asset space with unwavering commitment to timely, relevant information.

Delivered every day.

- Insights that move markets

- 100,000 active subscribers

Will Bitcoin reach $250,000 by December 31, 2026?