Difficulties in Digital Asset Valuation

Economic modeling is an important part of business planning that can give insights into the aggregate expenses and expected returns of a business venture and thus makes a projection about future developments, such as the venture’s growth curve. As you can imagine, this becomes increasingly important whenever the business needs to convince investors to support the business, such as before funding rounds or when going public. This ultimately helps investors determine the value of equity shares.

The same rules apply for valuing crypto tokens, regardless of whether it is for a seed-funding round, further funding, or for publicly traded tokens. However, token valuation can be tricky sometimes as most classical models fail to cover the dynamics of the token economy. Traditional businesses operate on a simple for-profit model: essentially, the shareholders pre-finance a venture and distribute the profits among themselves. This makes it possible to evaluate the shares based on the forecasted cash flows.

In contrast, crypto ventures rather operate on the principles of a sharing economy, where it is often unclear which parties generate some kind of economic value through the crypto network. Oftentimes, value accumulation for cryptocurrencies or utility tokens come about through increasing demand. It is therefore more important to identify the drivers of token value. For example, the value of “hard” cryptocurrencies that were designed primarily as a payment method, is mainly driven by the ability to pay with the currency. In other words, the main question one should ask when valuing these is “Will more vendors start accepting this currency?”.

Note the future tense. When “valuing” tokens, you are not trying to find out a token’s current value, but its future one, as you already know the current value. It’s exactly what you pay for the token on an exchange. The well-known MV = PQ formula, used to determine the present value of a currency, doesn’t help us in that respect. Rather, MV = PQ is an attempt to rationalize the present value in retrospect, tied to the notion of the currency having some “intrinsic value”.

As any serious economist (that is, anyone who follows the teachings of the Austrian School) can tell, there is no such thing as intrinsic value. The value of any asset, be it physical or digital, is always the amount of money that other people are willing to pay for that asset. The important question to ask is whether people are willing to pay more in the future. For hard cryptocurrencies, this is the case when more people start using and accepting the currency.

For utility tokens, the valuation process becomes more complex. Their demand and hence, their value, is driven by the very abstract concept of “utility”. Therefore, we need to ask the question, whether the token’s utility will increase in the future. This can be the case when more functionality is added to the underlying blockchain network, or when companies and DApps join the network’s ecosystem.

Valuing Cryptocurrencies as Investment Opportunities

When valuing digital assets, you should always compare them with all other assets available in the cryptoeconomy. Think of digital assets as investment vehicles. If you hold your assets in an Altcoin and the Altcoin increases in value, this can still turn out to be a bad investment if Bitcoin’s value rises at a faster rate. In this case, it would have been more profitable to invest in Bitcoin. This is also the reason why most investors prefer BTC as a reference currency, rather than the USD.

Let’s take a page from the playbook of cash flow valuation. Investors typically don’t settle with investments that have marginally positive cash flow after X number of years. This is because by putting money on the line, they forego other investment opportunities that might grant them a higher return. Therefore, investors apply an annual discount factor on the cash flow that reflects risk and the sacrifice of other investment opportunities. Only if the investment beats out this discount factor is it considered a good investment.

In total, this gives us a good qualitative approach to consider crypto investments. Let us take the example of a simple Proof of Stake coin that grants stakers an annual return of 10% by inflating the token pool. Here, the big unknown factor is the coin’s value projectory over time.

Nevertheless, this already allows stakers to make quantitative statements about their financial status one year in the future: under the assumption that the coin keeps its value in reference to USD, the investor has made a 10% return compared to holding his assets in USD. Likewise, under the assumption that the token keeps its value in reference to BTC, the investor has made a 10% return compared to holding BTC.

The investor might additionally apply a discount factor in order to account for risk and the various other investment opportunities both in traditional markets and crypto markets, such as lending or staking in decentralized finance. Therefore, in order to identify the coin as a good investment opportunity, she must predict that the coin’s value, in addition to her 10% return, beats out USD, BTC, and the discount factor.

Practical Example of Cryptocurrency Valuation

Looking at cryptocurrencies with the eyes of an investor, let us put this approach at token valuation to practice. Last month,Hashed team released a blog post that shared insights on the valuation model used for valuing Luna, one of the assets that is part of the Venture Fund’s Cryptocurrency portfolio. Under their dual-token model, Luna is used for block validation on their Proof of Stake blockchain and acts as a reserve for the Terra stablecoin.

Instead of inflating the Luna token pool as block rewards for validators, Terra levies a transaction fee of 0.5% on all stablecoin transactions, which is distributed to block producers. This means that we can identify actual cash flows that can be used to quantify the annual return on staking Luna tokens and, by proxy, the token’s value development.

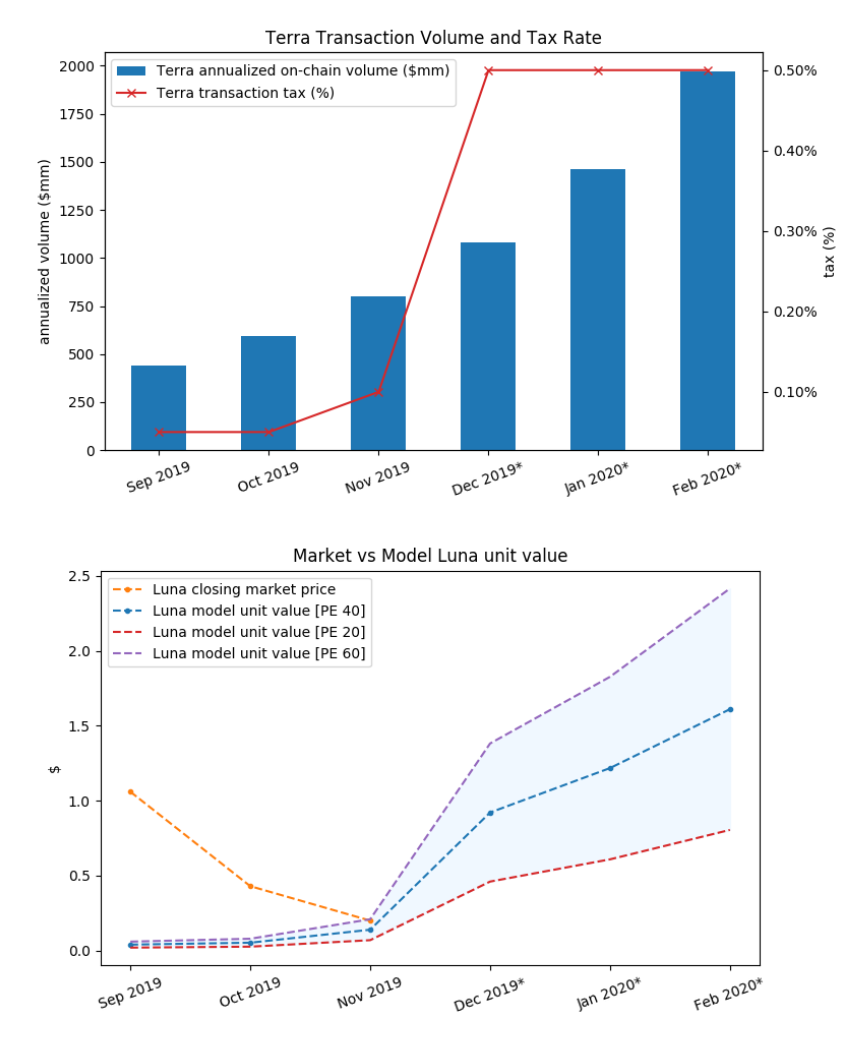

Terra’s annualized transaction volume has reached $800 Million in November with a steady monthly increase of 35% on average and Terra expects this trend to continue over the next few months. While Terra’s valuation model takes future trends into account, we will only focus on November’s numbers in this article, for the sake of brevity.

With an annual transaction volume of $800 Million and a 0.5% transaction fee, this means that $4 Million will be distributed to the 220 Million Luna that is currently staked. Stakers will, therefore, receive a return of roughly $0.0182 per Luna.

The open question that remains is how much investors would be willing to pay for one Luna to earn this yearly return. In a similar vein as traditional stocks traders, Terra uses the earnings multiple to arrive at a token valuation. The earnings multiple is the ratio between a stock price and the company’s annual earnings, or in other words, the number of years of consecutive earnings it would take for earnings to equal the stock price.

Terra believes that market equilibrium will ultimately settle the token price at an earnings multiple of 40, which is about on par with Visa and Mastercard. With expected annual earnings of $0.0182, this transfers into a price of $0.73 per Luna. Additionally, Terra sets the range for the eventual earnings multiple between 20 (worst case scenario) and 60 (best case scenario).

Top: Projected annualized transaction volume on the Terra blockchain. The transaction fee has been increased to 0.5% in December 2019.

Bottom: Projected token valuation at an earnings multiple of 20, 40, and 60.

Conclusion

The valuation of digital assets remains difficult as classical cash flow analysis is often not possible and the fundamental analysis of blockchain projects leaves many open questions. From an investor’s perspective, some qualitative statements can be made regarding the development of demand for utility tokens and cryptocurrencies. This makes the evaluation of investment opportunities, such as PoS staking possible.

Since Terra uses staking rewards based on cash flow instead of token inflation, it is possible to make quantitative statements about the annual staking rewards. Applying an earnings multiplier projects the development of the token price for Luna. The model could be refined by applying a discount factor to account for investment risks and the presence of competing for investment opportunities in the crypto economy.

About Author:

Jethro De Jager

Twitter: https://twitter.com/Javaeth

Bio: Part-Time Journalist and Java/Python Developer interested in developing his own dApp on Ethereum someday. In his free time, he learns to code using Solidity and critically reviews Blockchain startups

Why Trust CoinGape

CoinGape has covered the cryptocurrency industry since 2017, aiming to provide informative insights Read more… to our readers. Our journal analysts bring years of experience in market analysis and blockchain technology to ensure factual accuracy and balanced reporting. By following our Editorial Policy, our writers verify every source, fact-check each story, rely on reputable sources, and attribute quotes and media correctly. We also follow a rigorous Review Methodology when evaluating exchanges and tools. From emerging blockchain projects and coin launches to industry events and technical developments, we cover all facets of the digital asset space with unwavering commitment to timely, relevant information.

Delivered every day.

- Insights that move markets

- 100,000 active subscribers