Stablecoins Can Be More Profitable Than Altcoin Staking?

Cryptocurrency staking has exploded in popularity in the last year, as more cryptocurrencies than ever before now allow users to stake their assets in return for rewards paid out by the network.

Although altcoin staking can be profitable in many cases, a sizable fraction of stakers are currently suffering devastating losses, due to the underlying volatility of the asset they stake and/or the prevailing market conditions. For those with less of a risk appetite, stablecoin investments have emerged as a safer alternative to altcoin staking, since stablecoin holders can now net an impressive yield while taking on little to no risk while doing so.

Many Staking Coins Have a Negative APR

Although many cryptocurrencies boast high APRs, seemingly allowing holders to earn an impressive yield on their assets without little to no risk. The truth is, few cryptocurrencies actually produce a positive yield when you also consider the price action of the underlying asset. After all, what is the use of gaining 50% APR per year, when the underlying asset has fallen by significantly more?

Because this APR is measured in the underlying asset, not in terms of US dollar (USD) value, many stakers mistakenly believe they are turning a profit by staking their assets — when in reality, they are actually in the red. This is often the case when you look over the lifetime of an asset, rather than focusing on any short term changes in value.

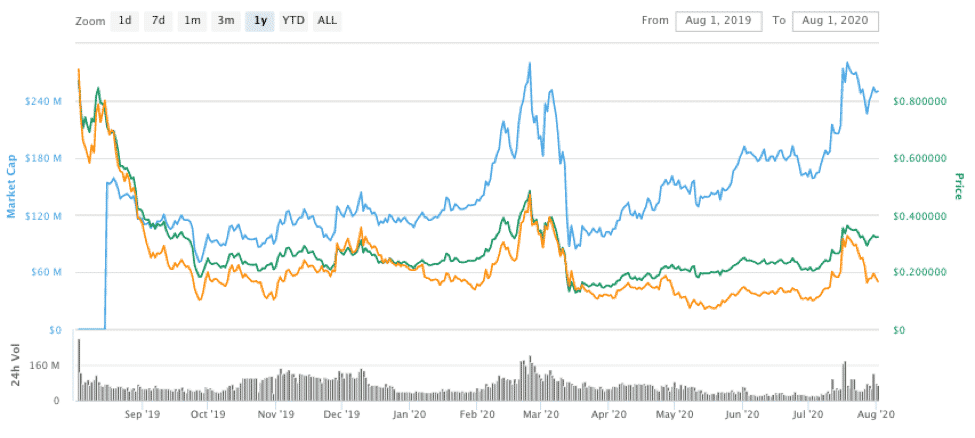

Take Algorand (ALGO) as an example. ALGO holders can currently earn around 5.1% APR for staking their tokens. However, as per data from CoinMarketCap, Algorand has seen its price collapse by almost 90% since it launched in June 2019 — the time when the vast majority of ALGO holders first acquired their tokens.

Overall, had you held ALGO from the date which staking rewards were first introduced (August 2019) and held until a year later (August 2020), you would have lost almost half of your money in terms of USD value — but you would have 5% more ALGO than you started with — not ideal.

As such, it’s important to consider the performance of the staked asset to calculate the true expected yield.

You Can Earn Yields Without Centralized Platforms

The ultimate goal of decentralized finance (DeFi) is to help individuals retake control of their finances by reducing or eliminating reliance on centralized financial institutions like banks, stock markets, and even governments.

However, while many DeFi projects have emerged in recent months — many of which have the sole aim of generating quick returns for investors — few actually have staying power, because the token behind many of these projects lacks real utility. Moreover, many DeFi protocols have been exploited in recent months, including DeFi lending platform Bzx which has been hacked three times this year and Balancer — which hacked twice in the span of 24 hours.

Likewise, although there are a large number of platforms that promise generous returns on cryptocurrency deposits, these platforms are almost always vulnerable to hacks and black swan events, which can cause total losses to users. This has made many firms cautious to launch DeFi platforms or accept their assets on their platform.

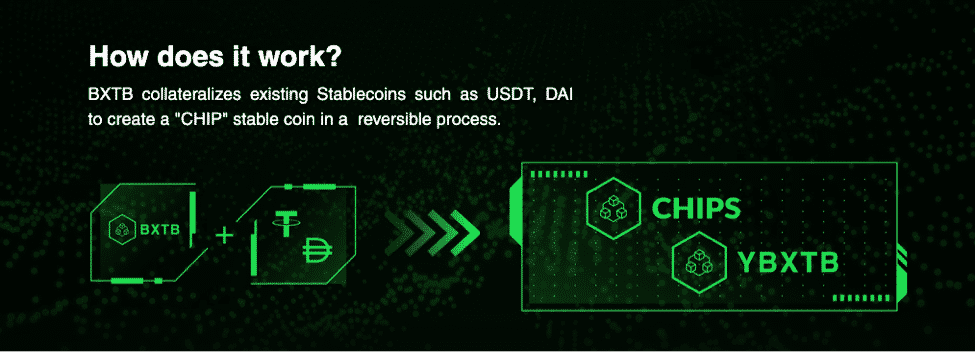

To help overcome DeFi’s current limitations and provide a secure yield-generating asset to market participants, BXTB launched an entirely new solution — the first yield-generating stablecoin solution, known as CHIP. Unlike other stablecoins which are backed by fiat currencies, CHIP is backed by other stablecoins, like DAI and Tether (USDT).

To create CHIP, users need to combine a second token known as BXTB with a supported stablecoin, to generate an equivalent number of CHIP tokens in addition to activated BXTB (yBXTB) — this is a reversible process, allowing users to get their original stablecoins back.

CHIP tokens are designed to remain pegged to the underlying stablecoin, whereas activated BXTB is the yield-generating asset. By holding yBXTB, users earn a share of revenues from transaction completed on the BXTB sidechain.

The Risks of Liquidity Pools

Liquidity pools are rapidly growing in popularity among cryptocurrency traders, since they allow traders to contribute their assets to a pool and earn a fraction of the fees generated when traders exchange their assets.

Although there are a wide array of decentralized exchange (DEX) platforms that allow users to contribute liquidity, Uniswap has emerged as by far the most successful, due to its ease-of-use, flexibility, and the seeming profitability of its liquidity pools. However, less experience liquidity providers need to watch out for impermanent losses (IL) — which can dramatically impact the value of assets stored in the liquidity pool.

The ETH-RARI pool is currently losing more to impermanent losses (-7.83%) than gained in fees per month (+1.93%). (Image: UniswapROI)

These impermanent losses occur when one side of a liquidity pool rapidly loses value compared to the other side. This can cause users who have a stake in the pool to lose significant sums — which are not covered by the fees earned for contributing liquidity. Because of this, Uniswap can be risky when providing liqudity for volatile assets that don’t have a long term bullish trajectory.

This can be largely avoided by contributing less volatile assets, or contributing to purely stablecoin liquidity pools on platforms like Curve.

Why Trust CoinGape

CoinGape has covered the cryptocurrency industry since 2017, aiming to provide informative insights Read more… to our readers. Our journal analysts bring years of experience in market analysis and blockchain technology to ensure factual accuracy and balanced reporting. By following our Editorial Policy, our writers verify every source, fact-check each story, rely on reputable sources, and attribute quotes and media correctly. We also follow a rigorous Review Methodology when evaluating exchanges and tools. From emerging blockchain projects and coin launches to industry events and technical developments, we cover all facets of the digital asset space with unwavering commitment to timely, relevant information.

Delivered every day.

- Insights that move markets

- 100,000 active subscribers

Will Bitcoin reach $250,000 by December 31, 2026?